Discover SMEs’ top risk concerns, and are they protected?

Vero’s 2022 SME Insurance Index Bonus Chapter, ‘Attitudes to Risk’, has revealed a number of key opportunities for brokers to deliver expert advice and to reinforce their role as risk advisers.

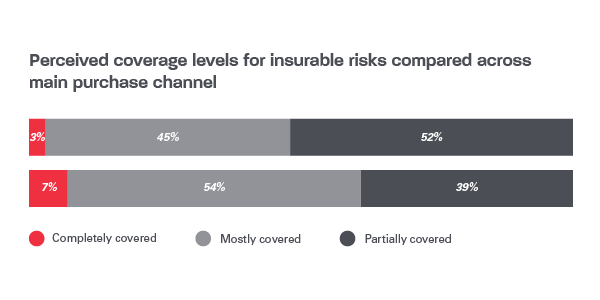

Perceived coverage levels differ based on how SMEs purchase their insurance.

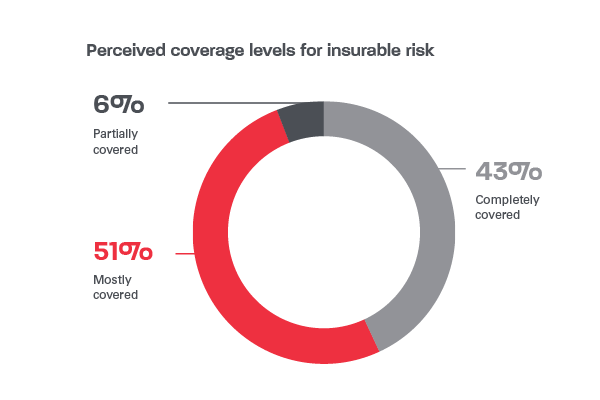

To uncover SMEs’ understanding in this area, this year we asked what their perceived cover levels are for their insurable business risks. The results showed 43% of respondents think that they are completely covered*, while 51% say that they are mostly covered and 6% admit to only being partially covered.

We can further see in the below graph, 52% of broker clients believe that they are completely covered for insurable business risks, compared to only 39% of direct buyers. This suggests that broker clients have a higher level of confidence than SMEs who buy direct.

The risk of underinsurance is real

Underinsurance is an area of concern for small businesses, which has only been exacerbated as general costs increase, businesses respond to supply chain challenges by holding higher stock levels and operating models evolve to meet changing circumstances. So why are some SMEs reducing insurance coverage? In a challenging economic environment, it's understandable a proportion of business owners have been looking to cut costs. Our data shows that only 37% of businesses with declining revenue are completely covered against a negative scenario, compared to 54% and 49% of businesses with no change in revenue and increased revenue respectively.

But is underinsurance fully understood?

As business owners grapple with seemingly never-ending uncertainty and business confidence continues to waver, cost cutting is to be expected. In fact, over half of SMEs say they aren’t completely covered for all business risks, and of those, a concerningly high number have no plan for what they would do if they experienced a major negative event.

Large businesses are at risk too. Though they are more likely to have contingency plans in place, there are still almost 1 in 4 who haven’t thought about what would happen if they experienced a major negative incident.

Good risk management is good for business

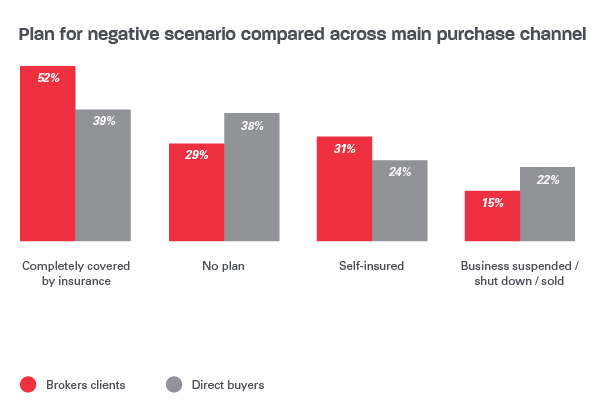

Brokers have a unique opportunity to help SMEs understand and devise risk mitigation strategies that help protect business success. The graph below shows that broker clients are far more likely to be completely covered against business risks, with 52% completely covered compared to 39% of direct clients.

Furthermore, only 15% of broker clients suspended business, shut down or were sold compared to 22% of direct buyers. This demonstrates that brokers can help SMEs have a more sophisticated understanding of the specific risks they face. Once SMEs understand the risks they face, brokers can help ensure they have relevant cover, as well as policies and procedures in place that put business security at the forefront of their operations. Being there for your SME clients as an insightful risk advisor helps them prepare for unexpected costs, which in turn, plays a key role in ensuring their success.

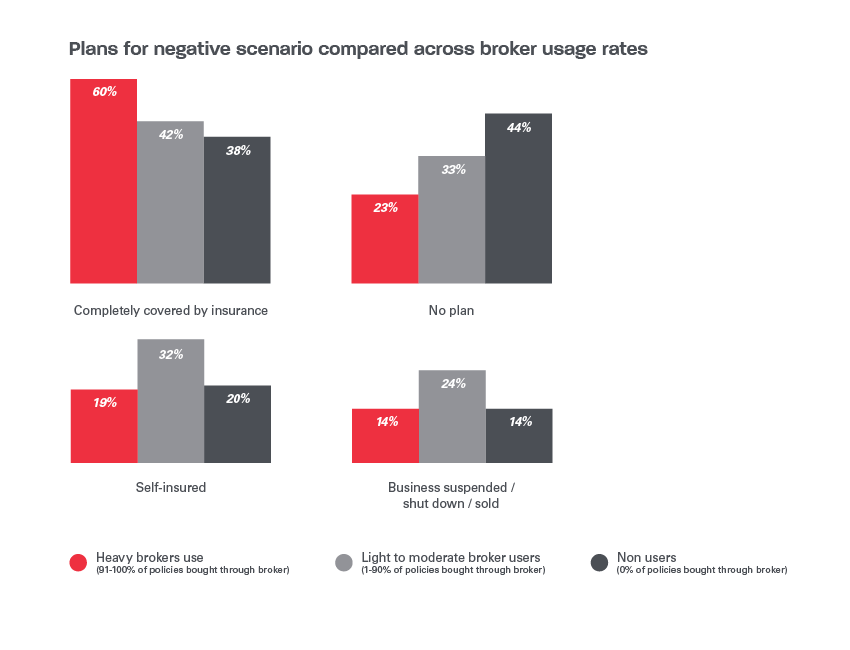

Additionally, the graph below shows that heavy broker users are also far more likely to be covered and have a plan in place for a major negative incident.

See good risk management in action

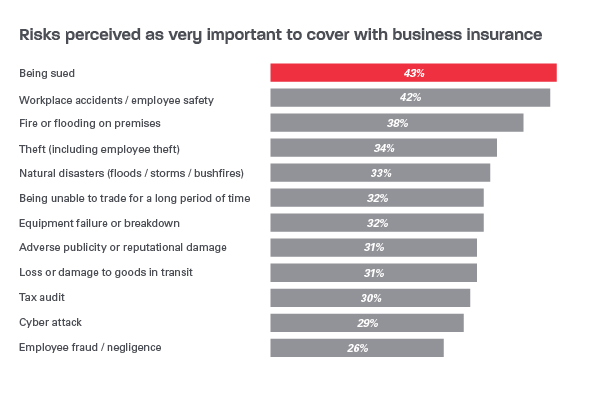

SMEs top concerns

SMEs are concerned about a large range of risks, at the top of the list are relatively widespread scenarios: being sued, workplace accidents, fire or flooding, theft and natural disasters. However, a significant number of SMEs are concerned about more specialized risks. For example, 31% say it is important to be covered for loss or damage to goods in transit and 29% want to be covered for cyber-attack. Brokers have an advantage in being able to offer a wide range of specialised risk products and advice.

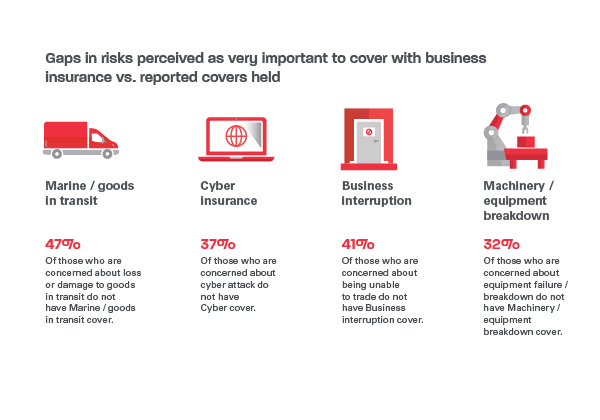

The gaps in concern and coverage

There are significant gaps between the number of SMEs who are concerned about risks and those reporting they have relevant cover. For example, almost half of SMEs concerned about loss or damage to goods in transit lack relevant cover. Notable gaps in coverage were also identified amongst risks such as cyber-attack, the inability to trade and machinery breakdown.

The gaps in concern and coverage

This represents an opportunity for brokers to educate SMEs about the potential to provide for these risks as part of a broader risk mitigation strategy. Brokers can educate clients about cover types, to help them understand what is available and how it could benefit their business. More generally, brokers could consider ensuring that their clients have an overall awareness of the risks that they face and initiate discussions around whether their cover is sufficient.

To see the full risk findings and what they mean for brokers download the 2022 Vero SME Insurance Index Risk Bonus Chapter and the SME Insurance Index Risk Infographic

For more actionable insights download the full SME Insurance Index Report and Infographic

Or, register to watch the webinar on-demand and gain 1 CPD point: Vero SME Insurance Index Webinar

* "Completely covered” refers to the survey respondents’ personal perception of how well they think that they are covered for their insurable business risks. This result in no way measures the respondents’ actual coverage levels.

Source: The SME Insurance Index report research was conducted by BrandMatters. See www.brandmatters.com.au

The information displayed is based on commissioned research involving 1,500 SME and 100 large business owners and decision-makers from around Australia. The research was conducted in October 2021. AAI Limited ABN 48 005 297 807 trading as Vero Insurance (Vero) has prepared this Vero SME Insurance Index Report (Report) for general information purposes only. Vero and its related bodies corporate do not assume or accept any liability whatsoever (including liability for special, indirect, consequential or incidental damages, or damages for loss of profits, revenue or loss of use) arising out of or relating to this Report or the information it contains. Vero and its related bodies corporate do not invite reliance upon or accept responsibility for the information it provides on or through this Report. Vero and its related bodies corporate do not give any guarantees, undertakings or warranties concerning the accuracy, reliability, completeness or currency of the information provided. This Report is not a recommendation or statement of opinion about whether a reader should acquire insurance from Vero (or its related bodies corporate) or services from any insurance intermediary or otherwise alter their business arrangements. This Report is based on commissioned research by Vero and should not be used as the basis for any decision in relation to the acquisition or disposal of insurance products or the use of broker services. Readers should confirm information and interpretation of information by seeking independent advice.